Examine the evolving pattern of Centre-State financial relations in the context of planned development in India. How far have the recent reforms impacted the fiscal federalism in India?

Examine the evolving pattern of Centre-State financial relations in the context of planned development in India. How far have the recent reforms impacted the fiscal federalism in India?

Centre-State financial relations in India, provided under Articles 264–293, define the distribution of taxation powers, grants, borrowing authority, and resource allocation. These relations have continuously evolved with India’s shift from a centralised planned economy to a liberalised system, and more recently to a cooperative federal structure under reforms like GST and Finance Commission devolution.

Evolution of Centre-State Financial Relations in Planned Development

Economic reforms Pre and Post Niti Aayog

Centralised Planning Era (1950–1991):

- Planning Commission dominated fiscal relations, allocating resources through the Gadgil formula.

- States remained dependent on discretionary central transfers and loans under Article 282.

- National Development Council offered limited state participation but real power stayed with the Centre.

- This led to vertical fiscal imbalance, with states spending more but raising less revenue.

Post-1991 Liberalisation:

- With economic reforms, states gained greater autonomy in resource mobilisation.

- FRBM Act (2003) encouraged fiscal discipline and borrowing limits.

- Role of Finance Commissions increased, shifting devolution from plan to non-plan transfers.

- States began to attract foreign and private investment, reducing sole dependence on Centre.

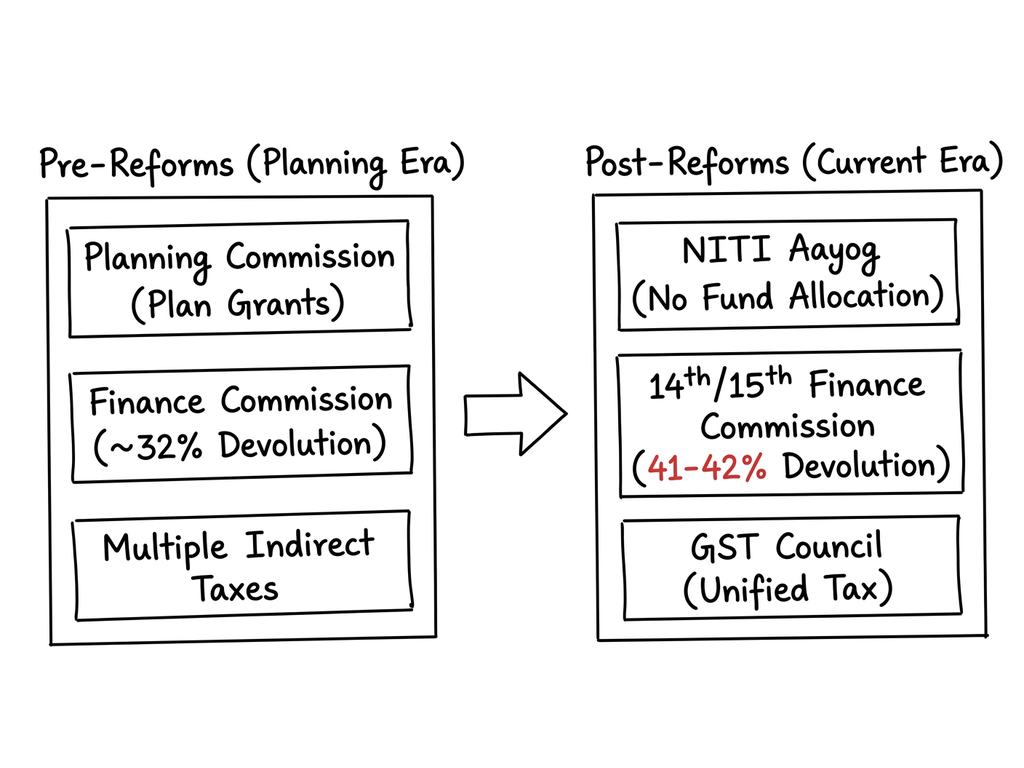

Impact of Recent Reforms on Fiscal Federalism

| Reform Area | Earlier Framework | Post-Reform Impact |

|---|---|---|

| Taxation | Fragmented indirect tax structure | GST (2017): Unified regime with GST Council as institutional forum |

| Planning | Planning Commission (centralised) | NITI Aayog (2015): Cooperative, consultative approach |

| Tax Devolution | 32% (13th FC) | 41% (15th FC): Higher untied resources for states |

| Borrowing | Strict central control | FRBM revisions & Atmanirbhar Bharat: Relaxed borrowing limits |

Positive Outcomes

- GST Council institutionalised fiscal federalism through joint decision-making.

- Higher tax devolution (41%) provided more flexibility and autonomy.

- Performance-based grants incentivised reforms in power sector, population management, and urban local bodies.

- DBT and digital reforms improved efficiency and reduced leakages, empowering states in welfare delivery.

Challenges Persist

- Vertical fiscal imbalance remains—states incur ~60% expenditure but raise ~40% revenues.

- Centrally Sponsored Schemes (CSS): Conditional transfers restrict true autonomy despite higher devolution.

- GST compensation disputes (post-2020) created tensions, especially during pandemic revenue shortfalls.

- Rising state debts and off-budget borrowings have strained fiscal stability (e.g., Kerala, Punjab).

Going forward, reforms could include raising states’ tax share beyond 41%, ensuring statutory GST compensation, rationalising Centrally Sponsored Schemes, and linking borrowing limits with fiscal discipline. Overall, fiscal federalism reflects a blend of flexibility and central oversight, ensuring national cohesion while steadily empowering states.

Answer Length

Model answers may exceed the word limit for better clarity and depth. Use them as a guide, but always frame your final answer within the exam’s prescribed limit.

In just 60 sec

Evaluate your handwritten answer

- Get detailed feedback

- Model Answer after evaluation

Model Answers by Subject

Crack UPSC with your

Personal AI Mentor

An AI-powered ecosystem to learn, practice, and evaluate with discipline