Comment on the important changes introduced in respect of the Long term Capital Gains Tax (LCGT) and Dividend Distribution Tax (DDT) in the Union Budget for 2018-2019.

Comment on the important changes introduced in respect of the Long term Capital Gains Tax (LCGT) and Dividend Distribution Tax (DDT) in the Union Budget for 2018-2019.

The Union Budget 2018-19 introduced landmark reforms in capital gains and dividend taxation, fundamentally reshaping India's investment tax landscape and aligning it with global practices.

Equity Taxation Changes Budget 2018 19

Long-term Capital Gains Tax (LCGT) Changes

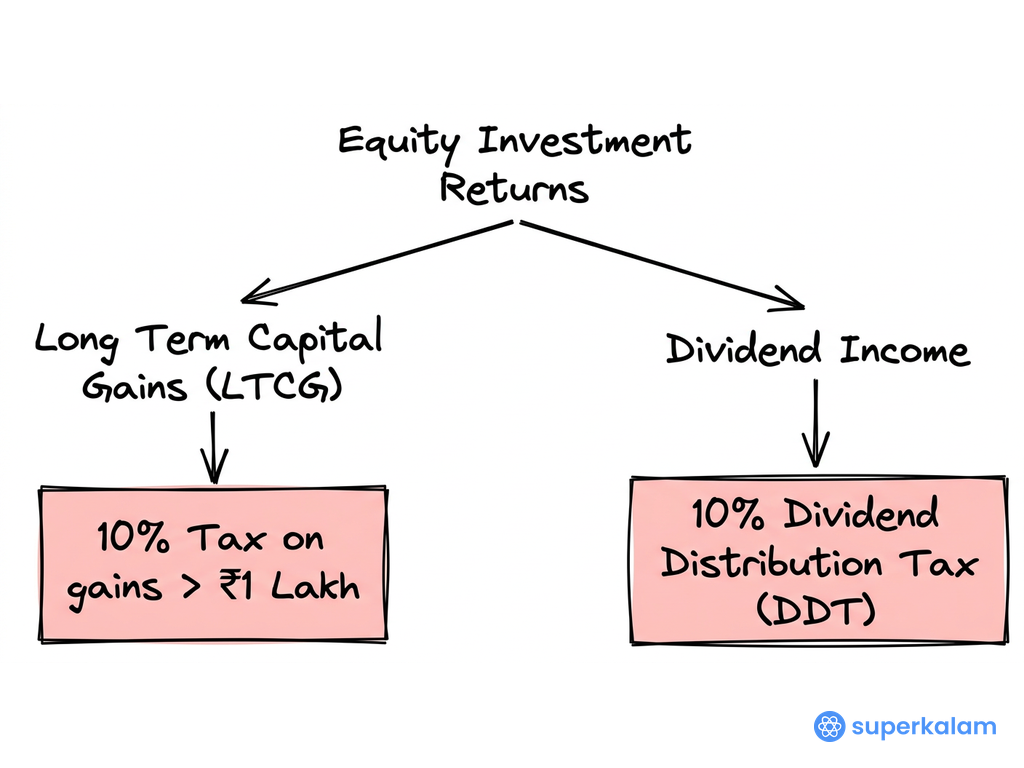

- Section 112A Introduction: Imposed 10% tax on LTCG exceeding ₹1 lakh from listed equity shares and equity-oriented mutual funds, ending the era of tax-free equity gains

- Grandfathering Provision: Protected all gains accumulated until January 31, 2018, from retrospective taxation, safeguarding existing investor interests

- Indexation Benefit Removal: Eliminated indexation benefits, simplifying tax calculations but potentially increasing effective tax burden for long-term investors

- Revenue Generation: Expected to generate approximately ₹20,000 crores annually while maintaining investment attractiveness

- Market Stability: Implementation with adequate transition period minimized market disruptions and investor panic

Dividend Distribution Tax (DDT) Reforms

- Classical Taxation System: Shifted from company-level DDT (approximately 20.56%) to individual-level taxation at applicable slab rates

- TDS Mechanism: Introduced 10% TDS on dividend payments exceeding ₹5,000 annually, enhancing tax compliance and collection efficiency

- Progressive Tax Structure: High-income investors now pay higher rates while lower-income investors benefit from reduced tax burden

- Foreign Investment Boost: Enabled foreign investors to claim tax credits in home countries, eliminating double taxation issues

- Corporate Benefit: Reduced compliance burden on companies while improving their cash flows by eliminating DDT payments

Impact and Implications

| Aspect | LCGT Changes | DDT Reforms |

|---|---|---|

| Revenue Impact | ₹20,000 crores additional | Neutral to positive |

| Investor Category | All equity investors | High vs. low income differential |

| Global Competitiveness | Maintained with exemption | Significantly improved |

| Compliance | Simplified | Enhanced through TDS |

These reforms represent a balanced approach between revenue generation and investment promotion, ensuring India's continued attractiveness as an investment destination while building a more equitable and transparent tax system aligned with international standards.

Answer Length

Model answers may exceed the word limit for better clarity and depth. Use them as a guide, but always frame your final answer within the exam’s prescribed limit.

In just 60 sec

Evaluate your handwritten answer

- Get detailed feedback

- Model Answer after evaluation

Model Answers by Subject

Crack UPSC with your

Personal AI Mentor

An AI-powered ecosystem to learn, practice, and evaluate with discipline