PM MUDRA Yojana 2025: Shishu to Tarun [UPSC Notes]

Dec, 2025

•4 min read

The Pradhan Mantri Mudra Yojana (PMMY) is a key government initiative designed to support small entrepreneurs and promote financial inclusion. It helps micro and small businesses access collateral-free loans, playing a crucial role in boosting self-employment, entrepreneurship, and grassroots economic growth.

The PM Mudra Yojana is a crucial topic for the Prelims (loan categories and beneficiaries) and Mains (role in financial inclusion, women's empowerment, and MSME growth). Let’s study this scheme in detail!

What is PM MUDRA Yojana?

The PM MUDRA Yojana is a flagship government scheme launched on April 8, 2015, by Prime Minister Narendra Modi. It operates on the philosophy of "Fund the Unfunded." The scheme provides collateral-free loans to small and micro-entrepreneurs who lack access to formal banking channels.

- Operates under the Ministry of Finance, Government of India.

- The scheme works through MUDRA, a government institution that supports and refinances loans for small businesses.

- Loans are given without collateral, so small entrepreneurs do not need to pledge assets to get finance.

- MUDRA (Micro Units Development and Refinance Agency Ltd) is a Non-Banking Financial Company (NBFC) providing refinance support.

- The scheme supports individuals and small businesses, with special focus on women entrepreneurs and SC/ST/OBC beneficiaries.

- Over 52.5 crore loans worth ₹33.65 lakh crore sanctioned since launch.

- Tamil Nadu (₹3.23 lakh crore), followed by Uttar Pradesh and Karnataka, are the top disbursing states.

Also read: Prime Minister Dhan-Dhaanya Krishi Yojana

Objectives of PM Mudra Yojana

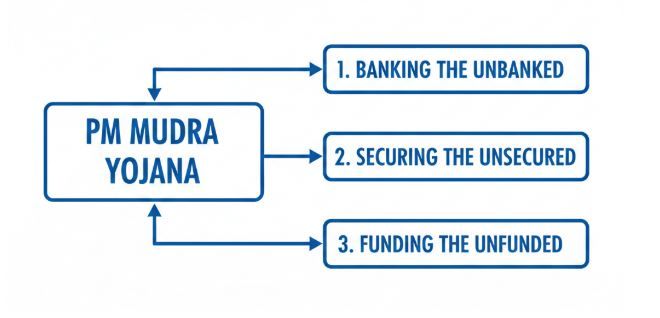

The PM Mudra Yojana is built on three foundational pillars of financial inclusion, each addressing a critical gap in India's credit ecosystem.

- Banking the Unbanked: Bringing formal financial services to people traditionally excluded from the banking system.

- Securing the Unsecured: Providing credit without collateral requirements to those unable to access traditional institutional lending.

- Funding the Unfunded: Bridging the credit gap for small entrepreneurs who face rejection from formal lenders due to a lack of collateral and business track record.

Also read: Make in India UPSC Notes: Pillars, Objectives, and Key Infrastructure Schemes

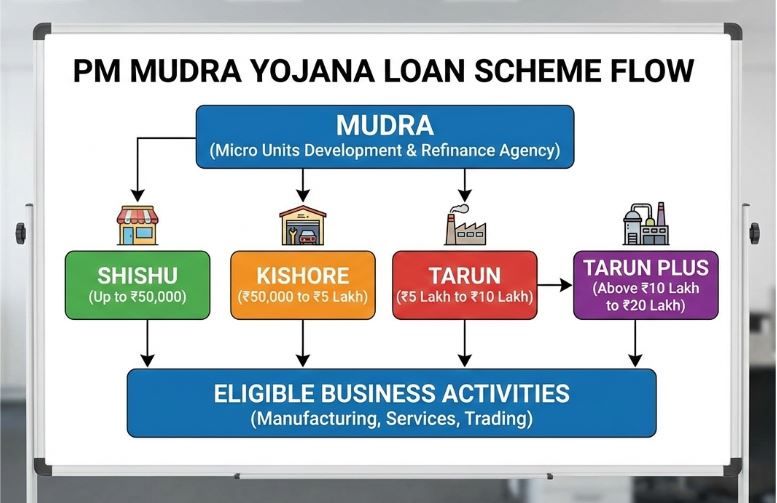

Mudra Loans Under PM MUDRA Yojana

The scheme uses a growth-stage approach, categorising loans into four distinct categories based on business maturity and funding requirements.

1. Shishu Mudra Loans (Up to ₹50,000):

- Designed for brand-new entrepreneurs and first-time business starters.

- Covers basic startup funding needs and working capital.

- Simplest application process with minimal documentation.

2. Kishor Mudra Loans (₹50,001 to ₹5 lakh):

- Meant for entrepreneurs looking to expand and scale their existing businesses.

- Provides growth capital for enterprises that have progressed beyond the startup stage.

- Used for equipment purchase, inventory expansion, and operational scaling.

3. Tarun Mudra Loans (₹5,01,000 to ₹10 lakh):

- Designed for well-established micro enterprises ready for significant expansion.

- Supports major capital investments and technology upgrades.

- Growing traction: evidence of enterprises achieving maturity.

4. Tarun Plus Mudra Loans (₹10 lakh to ₹20 lakh):

- A new category has been announced in the Union Budget 2024-25.

- Exclusively for entrepreneurs who have successfully availed and repaid Tarun loans.

- Represents graduation to a higher credit tier after demonstrating repayment discipline.

Maximum loan limit under PMMY.

Also read: Inclusive Growth UPSC Notes: Definition, Objectives and Government Schemes

PM MUDRA Yojana vs PM Jan Dhan Yojana

PM Mudra Yojana (PMMY) and Pradhan Mantri Jan Dhan Yojana (PMJDY) are both key financial inclusion schemes, but they serve different purposes. While Jan Dhan focuses on bank account access, Mudra focuses on credit for small businesses.

| Aspect | PM Mudra Yojana (PMMY) | PM Jan Dhan Yojana (PMJDY) |

|---|---|---|

| Year of launch | 2015 | 2014 |

| Main objective | Provide collateral-free loans to micro and small entrepreneurs. | Provide universal access to bank accounts |

| Nature of support | Credit (loans) | Banking access (savings account) |

| Beneficiaries | Small business owners, self-employed persons | Unbanked population, especially poor households |

| Loan facility | Yes (up to ₹20 lakh) | No regular loan (only a small overdraft facility) |

| Collateral requirement | No collateral required | Not applicable |

| Focus area | Entrepreneurship and self-employment | Financial inclusion and basic banking |

| Implementing institutions | Banks, NBFCs, MFIs through MUDRA | Banks and financial institutions |

| Role in the economy | Promotes MSMEs and job creation. | Brings people into the formal banking system. |

In short, Jan Dhan provides people with a bank account, while Mudra offers them funds to start or expand a business.

Also read: MSMEs in India UPSC Notes: Classification, Sectors and Government Schemes & Challenges

Achievements of PM MUDRA Yojana

The PM MUDRA Yojana stands as one of India's most successful financial inclusion initiatives, delivering transformative results for millions of entrepreneurs.

1. Overall Performance (As of March 2025):

- Loans Sanctioned: Over 52 crore loans worth ₹32.61 lakh crore since April 2015.

- Women Borrowers: A total of ₹ 8.49 lakh crore was disbursed under the Shishu category, ₹ 4.90 lakh crore under Kishor, and ₹ 0.85 lakh crore under the Tarun category.

2. Financial Inclusion Revolution:

- Women Entrepreneurs: 68% of all Mudra beneficiaries are women.

- Marginalised Communities: SC, ST, and OBC entrepreneurs account for 50 per cent of Mudra accounts.

3. MSME Sector Strengthening:

- Credit Flow Surge: MSME lending surged from ₹8.51 lakh crore in FY14 to ₹27.25 lakh crore in FY24, and is projected to cross ₹30 lakh crore in FY25.

- Market Share Expansion: MSME credit share in total bank credit rose from 15.8% (FY14) to 20% (FY24).

4. Employment Generation:

- Direct Impact: Widespread job creation at the micro-enterprise level across all sectors.

- Multiplier Effect: Employment generation through women-led MSMEs is particularly strong in states with higher female disbursement.

5. International Recognition:

The International Monetary Fund (IMF) has consistently recognised MUDRA's impact:

- 2017: Acknowledged scheme as instrumental in enabling women-led businesses to access finance.

- 2019: Praised MUDRA's role in developing and refinancing micro enterprises.

- 2023: Highlighted that women-owned MSMEs exceed 2.8 million due to PMMY.

- 2024: Reaffirmed that PMMY contributes to increased self-employment and formalisation through credit.

UPSC Prelims PYQ on PM MUDRA Yojana

QUESTION 1

Easy

Social Issues & Schemes

Prelims 2016

Pradhan Mantri MUDRA Yojana is aimed at -

Select an option to attempt

Challenges Faced by PM MUDRA Yojana

While the Pradhan Mantri Yojana stands as a remarkable success, like any large-scale financial inclusion scheme, it faces significant challenges that need continuous attention and refinement.

- High NPA Rate: NPA rate for Scheduled Commercial Banks under PMMY reached 9.81% as of March 2025, up from 5.47% in March 2018.

- Informal Use of Funds: Sometimes, loans meant for business establishment are diverted for personal consumption or other purposes.

- Inconsistent Monitoring: Lack of standardised procedures for tracking microentrepreneur performance.

- Category Shifting Issues: Frequent and improper transition of borrowers between loan categories leads to inaccurate performance assessment.

- Lack of Business Training: Borrowers often lack essential business management, financial literacy, and record-keeping skills.

- Limited Skill Development: Insufficient integration with skill development programs like NSDC.

- Sectoral Issues: Specific sectors face structural challenges affecting loan viability (e.g., retail affected by e-commerce).

- Sector Over-Concentration: Some sectors become overcrowded with multiple small businesses competing fiercely.

UPSC Mains Practice Question

Financial inclusion schemes like Pradhan Mantri Jan Dhan Yojana and Pradhan Mantri Mudra Yojana have expanded access to credit but raised concerns on asset quality and over‑indebtedness. Critically examine

Evaluate Your Answers nowWay Forward

The PM MUDRA Yojana needs better planning and support to solve current problems and fully achieve inclusive growth.

- Launch targeted digital campaigns in rural and semi-urban areas using radio, local media, and grassroots organisations.

- Partner with panchayats and self-help groups (SHGs) for on-ground awareness and assistance.

- Link MUDRA borrowers with NSDC skill development programs for sectoral expertise.

- Implement fully digital loan applications to reduce processing time to below 15 days.

- Establish early warning systems to identify struggling borrowers and provide support.

Unlock your UPSC Success with SuperKalam

Get instant doubt clearance, customised study plans, unlimited MCQ practice, and fast Mains answer feedback.

Join thousands of aspirants learning with India’s AI-powered mentor today!