GS 2: International RelationsGS 3: EconomyGS 3: Environment & Ecology

Keeping India’s carbon money at home, Pg6

India considers IBAM to counter EU's CBAM, aiming to retain carbon revenues for domestic green projects and ensure fair trade.

Practice MCQs

782 Students attempted

Key Highlights:

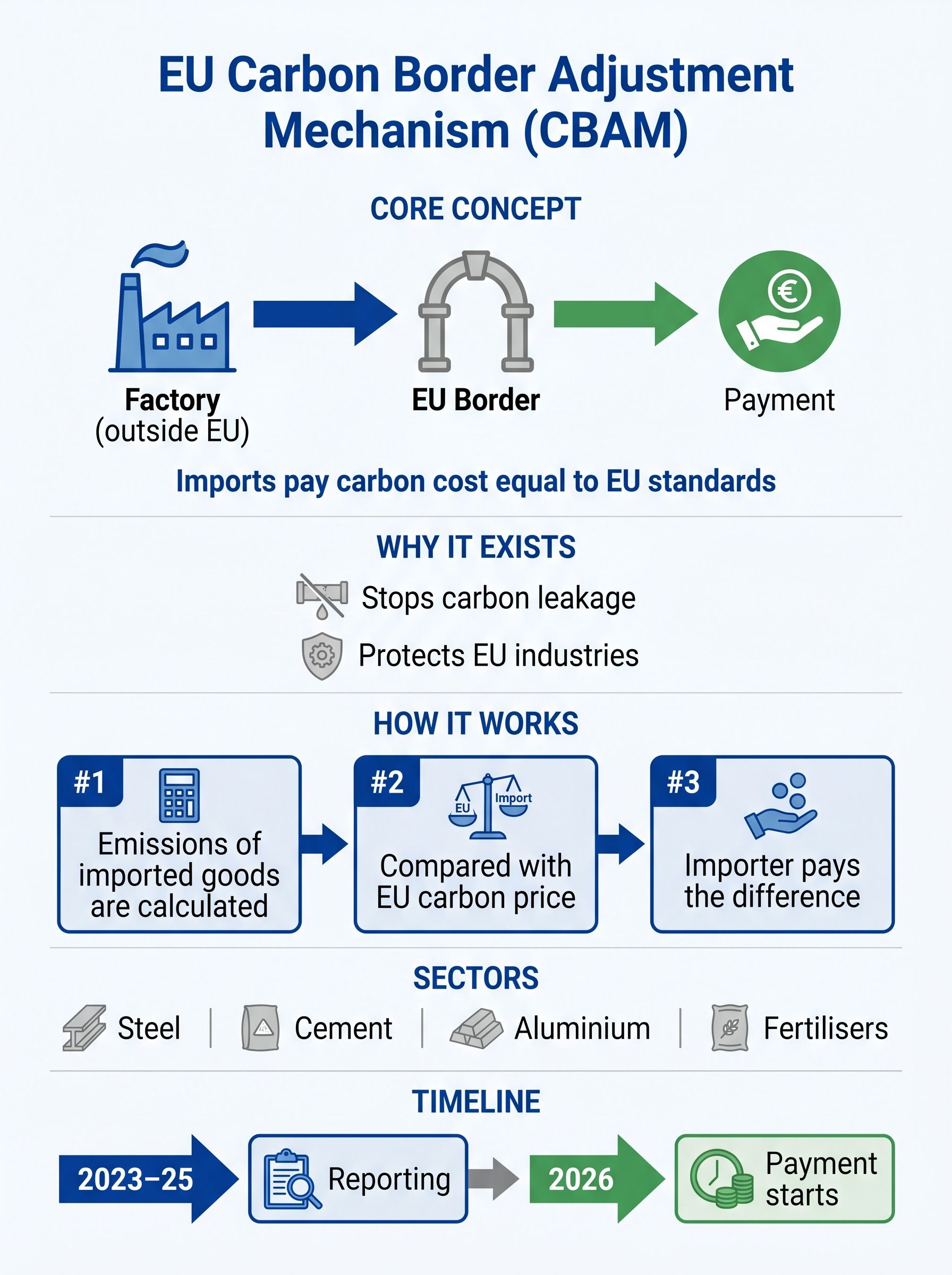

- The EU's Carbon Border Adjustment Mechanism (CBAM), effective since January 1, 2026, imposes carbon pricing on imports.

- The India-EU Free Trade Agreement (FTA), concluded on January 27, 2026, does not exempt India from CBAM.

- India's Carbon Credit Trading Scheme (CCTS), notified in 2023, establishes a domestic carbon price.

- India is considering an India Border Adjustment Mechanism (IBAM) to retain carbon revenues domestically.

Detailed Insights:

- CBAM impacts Indian exporters by imposing carbon charges without equivalent state support, unlike European producers who receive decarbonisation subsidies.

- The FTA's Annex 14-A establishes a technical dialogue on CBAM implementation, potentially allowing recognition of India's carbon price at the EU border.

- Climate justice is a key concern, as CBAM shifts the decarbonisation burden to developing countries while retaining revenue in Europe.

- CCTS allows European importers to deduct emissions that have already borne a carbon price in India, providing a legal basis for offsetting CBAM.

- IBAM would impose a carbon-based charge on CBAM-covered exports, collected in India, with revenues used for domestic green projects.

- Implementing IBAM carefully, through Annex 14-A, can ensure its recognition as a carbon price paid in the country of origin under CBAM Article 9.

- IBAM revenues should be ring-fenced in a dedicated fund for verifiable green projects, subject to strict standards and independent audits.

Key Concepts Involved:

- Carbon Border Adjustment Mechanism (CBAM): A carbon tariff on imports based on the carbon intensity of their production.

- Carbon Credit Trading Scheme (CCTS): A domestic scheme establishing a carbon price through tradable certificates.

- India Border Adjustment Mechanism (IBAM): A proposed carbon-based charge on exports to retain carbon revenues in India.

CBAM

SuperKalam is your personal mentor for UPSC preparation, guiding you at every step of the exam journey.

Download the App

STUDY RESOURCES

CONTACT US

ⓒ Snapstack Technologies Private Limited