GS 3: Economy

Uneven growth, Pg6

India's industrial growth slows to 3%, a five-year low, despite manufacturing sector rebound; labor-intensive sectors contract, raising job concerns.

Practice MCQs

818 Students attempted

Key Highlights:

- Industrial growth for April-September 2025 was the slowest in five years, registering at just 3%.

- Q2 growth showed improvement at 4.1%, compared to 2% in Q1 of FY26.

- The manufacturing sector grew by 4.8% in September 2025, the second highest in FY26.

- Mining sector activity contracted in September 2025, Q2, and the first half of FY26.

- More than half of the 23 main manufacturing sub-sectors contracted in Q2 of FY26.

- The consumer non-durables sector has contracted for the last six consecutive quarters.

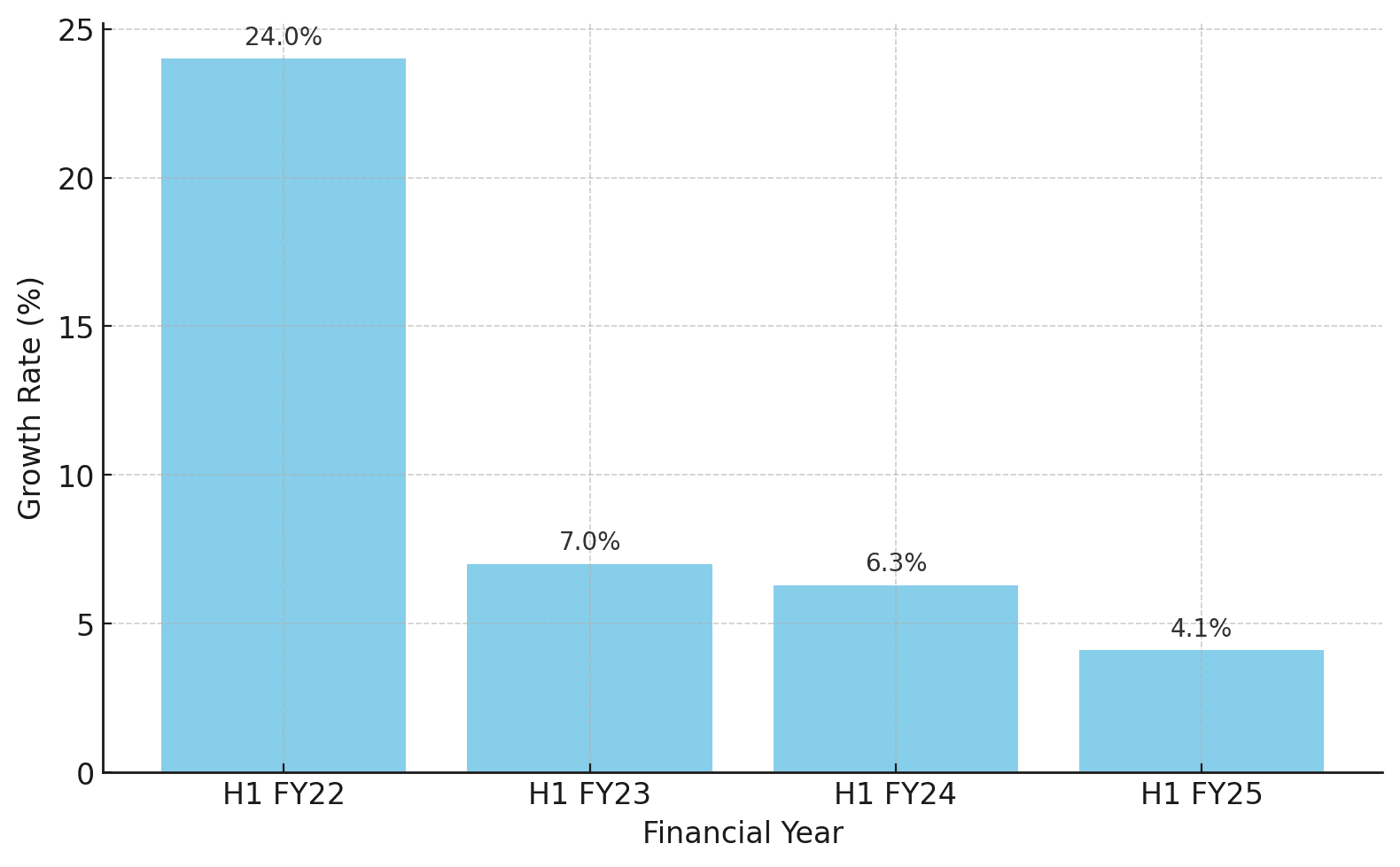

Half-Yearly (H1) IIP Growth Comparison — FY22 to FY25.png

Detailed Insights:

- Manufacturing sector's growth bounced back to 4.1% in April-September 2025, after slowing to 3.8% in the first half of the previous year.

- The July-September 2025 quarter saw the manufacturing sector grow by 4.9%, the fastest quarterly growth since the quarter ended December 2023.

- Contraction in the mining sector is attributed to the monsoon, but its performance remains unusually poor, requiring focus on energy and strategic mineral security.

- Growth in the manufacturing sector is not broad-based, with more than half of the 23 sub-sectors contracting in the July-September 2025 quarter.

- Labour-intensive sectors like apparels, leather, rubber, and plastics contracted in September 2025, potentially impacting job creation.

- Sectors that grew were mostly capital-intensive, including wood, mineral products, basic metals, and fabricated metal products.

- The contraction in the consumer non-durables sector reflects slack demand, which policymakers have been addressing, with the solution lying in increasing incomes and creating jobs.

Key Concepts Involved:

- Index of Industrial Production (IIP): An index that shows the growth rates in various industry groups of the economy in a specified period.

- Base Effect: The distortion in a monthly inflation figure caused by abnormally high or low levels of inflation in the year-ago month.

- Capital-Intensive Sectors: Industries that require a large amount of investment to produce a good or service.

SuperKalam is your personal mentor for UPSC preparation, guiding you at every step of the exam journey.

Download the App

STUDY RESOURCES

CONTACT US

ⓒ Snapstack Technologies Private Limited